We have had a few conversations with clients lately about what is happening in the US and the world from both an economic and geopolitical perspective. There is a lot happening in fairly rapid succession, some of which are causing the equity markets to become more volatile. While everyone likes volatility on the upside, no one enjoys the downside of volatility. I want to try to address some of your potential concerns by pointing you to a broader, longer-term look at investing.

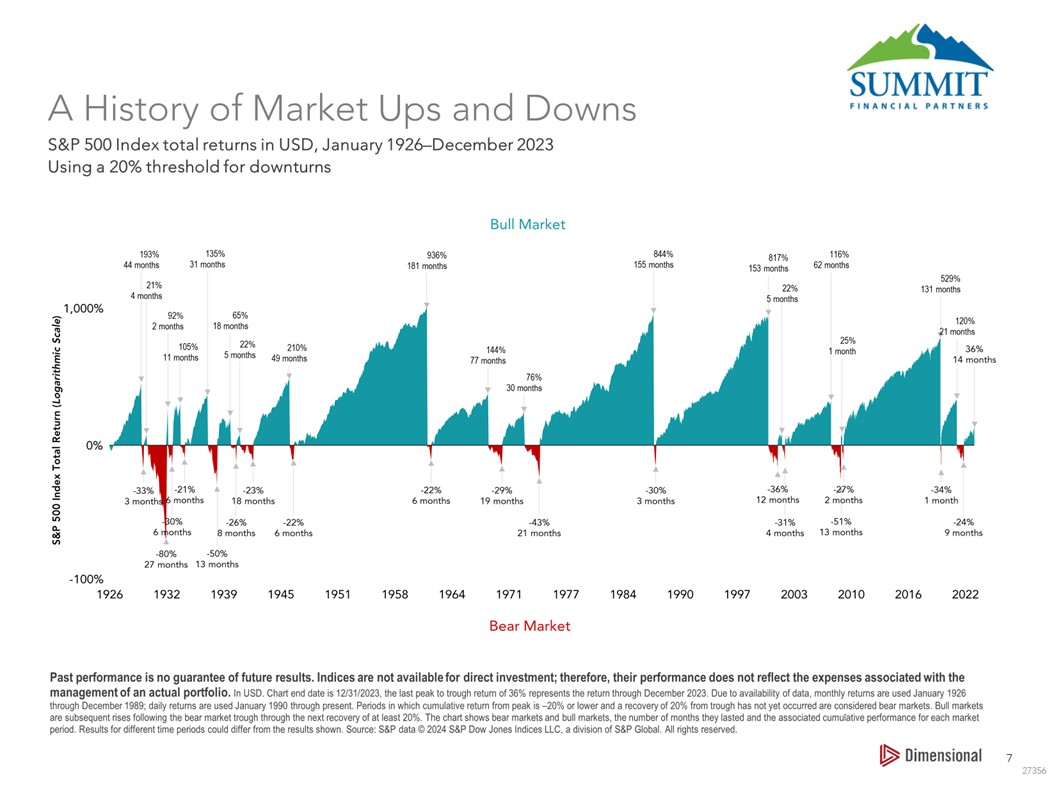

A History of Market Ups and Downs

First, let’s take a look at the historical performance of the S&P 500 since 1926, when the index first came into existence. As you can see, the markets are positive much more frequently and for longer periods of time than they are negative. Even the terrible Dot.com and Financial crisis look miniscule compared to the recoveries that happened afterwards. As I am sure you recall, those were both pretty terrible times where the economy was in shambles and people were losing their homes. Both periods were rough, with the Financial crisis of 2007-2009 being especially bad.

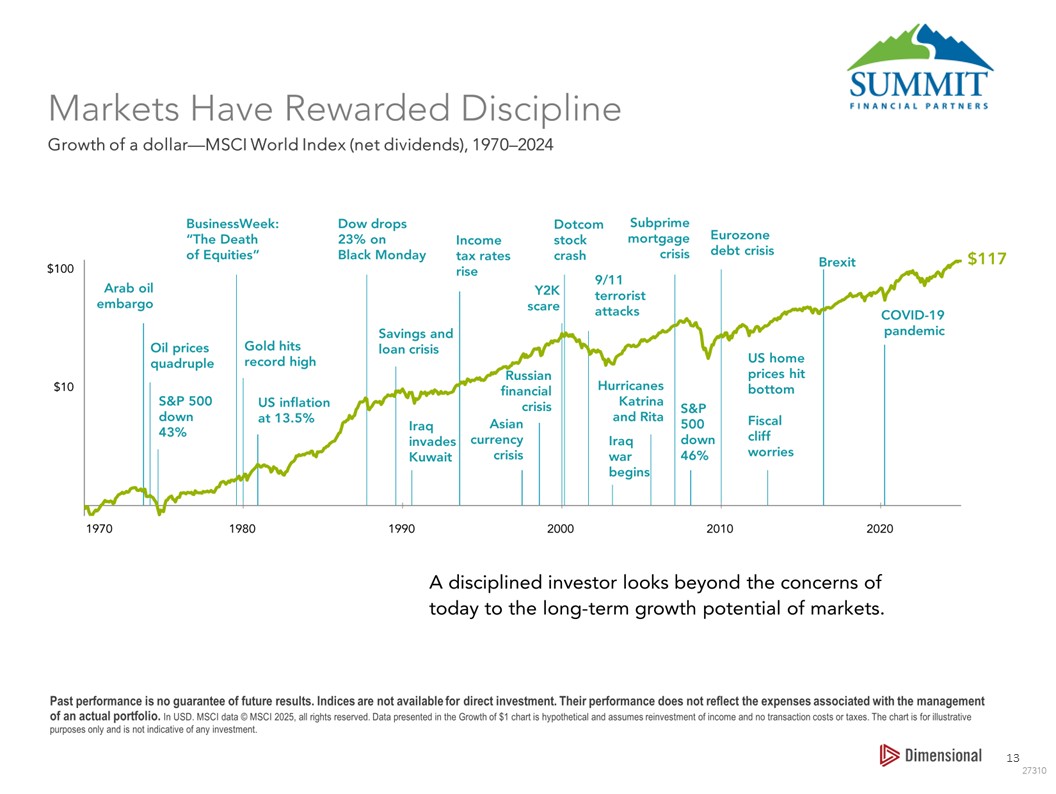

Markets Have Rewarded Discipline

Next, I want to address not only the long-term trend toward positive markets but also the comment we hear so often, “It is Different This Time.” This chart shows some of the great challenges that have happened over the last 50 years. And yes, each crisis was different, so the thought that “It is Different This Time” holds a lot of truth. However, through each challenge the market has either not had a downturn or recovered from a correction in a relatively short period of time. We have been through a lot in our lifetimes! What ultimately drives stock market performance in the long term, though, is whether companies are profitable. As long as the consumer continues to purchase and companies are well managed, stock prices will continue their upward trajectory. Unfortunately, it is not a straight line up, and at times we have to endure some “zags” with the “zigs.”

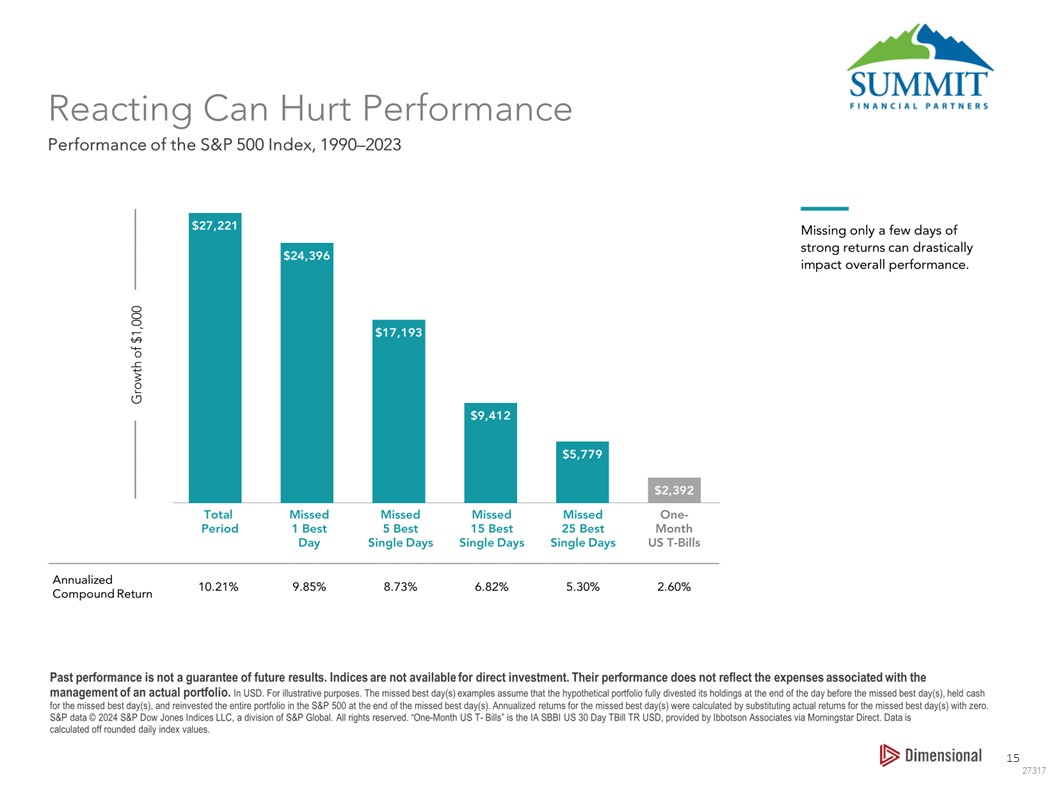

Reacting Can Hurt Performance

These last three graphs address the thought that many have of, “I have to do something!” Our brains are wired to react when something unsettling is taking place. It is part of the fight or flight phenomenon that happens in our amygdala. It is our body’s way of helping us stay safe. However, this reaction works against us when it comes to investing. Getting out of the stock markets often seems like the right move. Who wants to ride prices downwards? I don’t really enjoy it either, but there is risk in that move. Missing just a few of the best days of return can have huge consequences, as you can see the impact of missing the best days of returns over 25 years had on performance. Who would think that missing 25 days could reduce your return from 10.21% to 5.3%? That is enough to impact one’s standard of living.

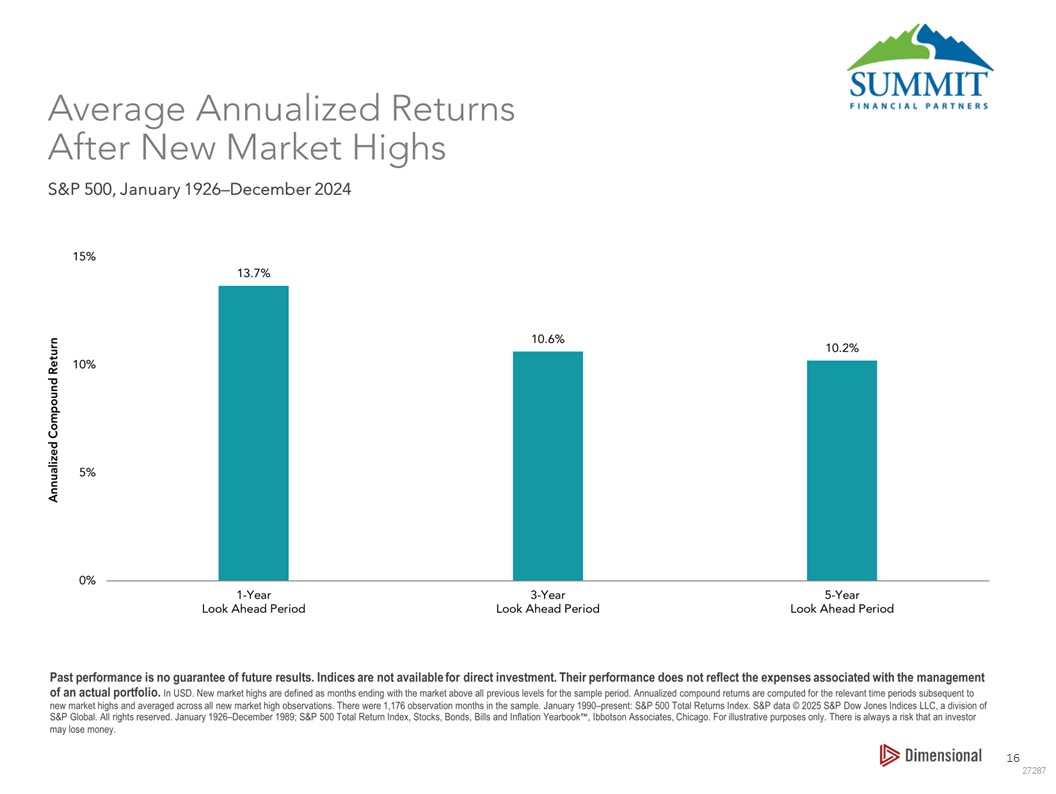

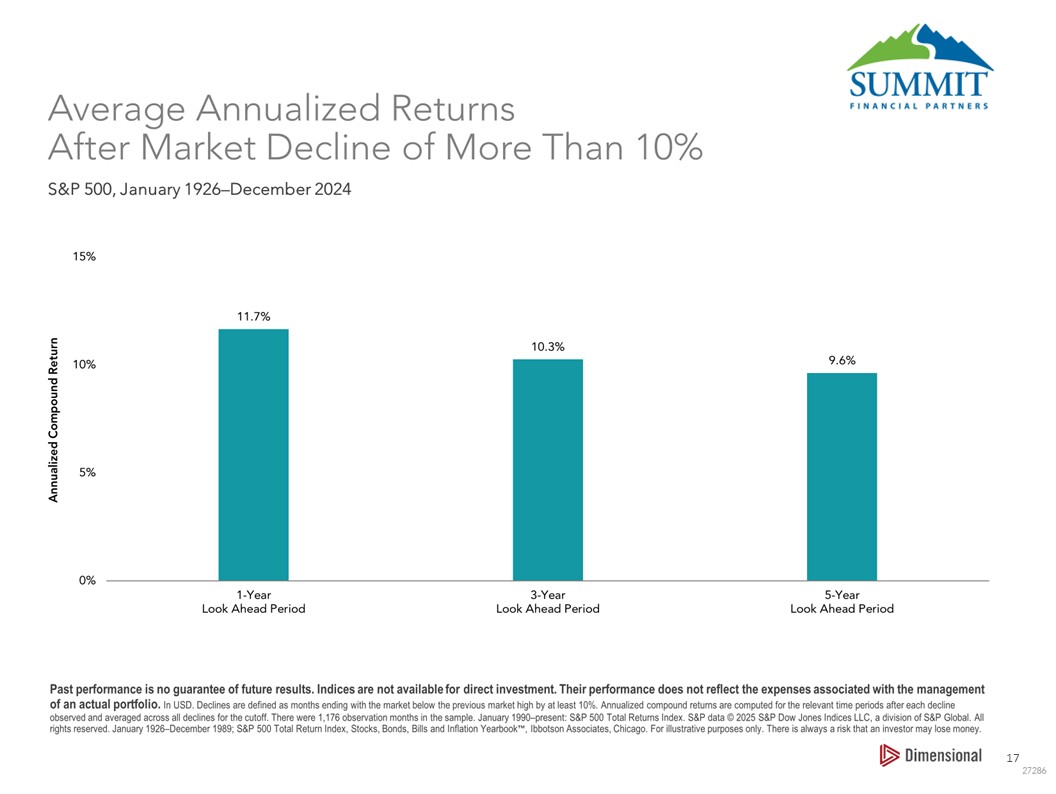

Humans also experience what is called “Recency Bias.” Recency Bias is when we expect whatever has happened recently will continue going forward. With investing it is assuming a negative market will not recover, at least not for a long, long time. We experience the flip side of that thought with positive markets, and that is when investors tend to get overconfident and take on risks they would not normally accept. The below graphs, though, show that positive markets tend to happen in the long run, no matter what we are currently experiencing.

Tariff Concerns

One concern that I do not have a graph for is tariffs. I share your concern that tariffs are a mighty big stick that is being used. Tariffs are a common tool for countries to use, but usually they are very stable. I am confident that the markets will adjust to the eventual settling down of tariffs, but we are likely going to have to endure some more volatility until that happens. The fact that companies exist to make profits and they are run by smart men and women gives me confidence that this landscape will eventually be navigated as well.

Dimensional recently held a live webcast on tariffs, Talking Top Stocks, Tariffs, and Tech. The webinar was recorded, and we will send you the recording as soon as Dimensional releases it!

Tune Out the Noise

Lastly, I encourage you to watch “Tune Out the Noise” about Dimensional. It is a movie, not a 20 minute clip, so you will need popcorn and your beverage of choice if you decide to watch it. It really is worth the time!

As always, we are here for you and are happy to talk through your concerns!

Best,

Jennifer

Jennifer

Want to chat more?

Want to chat more?

This article was originally written and published by Jennifer Luzzatto, CFA, CFP®, AIF®, CeFT® on the Summit Blog.